APAC Data Centre Investment Strategies in the Age of Digitalisation

July 2024

From 5G mobile to Zoom conferencing, and from TikTok to video streaming, global consumption and processing of digital products continue to accelerate, leading to surging demand for new data centre (DC) capacity for data to be stored and processed.

Executive Summary:

While cloud computing is today the primary driver for DC demand, the rise of artificial intelligence (AI) – both AI learning and applications – has become an additional demand driver. As operators prepare for an explosion in AI uptake, they have therefore embarked on a huge buildout of capital-intensive infrastructure to host the large number of specialised semiconductors the technology requires. In addition, there has been rapid expansion into peripheral locations able to offer both land and power resources required to accommodate escalating infrastructure needs.

The revolution in the scale at which data is being used and managed is fundamentally a global phenomenon, but nowhere is it unfolding as rapidly as in Asia Pacific (APAC) markets. Regional economies are not only growing faster and from a lower base, but they also have a cultural affinity for digitised business and technology adoption. In addition, the multitude of distinct regulatory jurisdictions across the region means data users must comply with a larger number of country-specific data protection policies compared to the West, driving a shift towards greater data localisation. Together, these factors are creating new opportunities for early-stage investment in what remains an emerging regional asset class.

Demand in the APAC region is equally strong for both dedicated and colocation DCs. Singapore, Tokyo, Osaka, Seoul, and Sydney are identified as key markets for new DCs, with the major Indian cities of Mumbai, Bengaluru and Chennai also showing promise due to growing digital services sectors, strong government support, and robust long-term economic prospects.

"The revolution in the scale at which data is being used and managed is fundamentally a global phenomenon, but nowhere is it unfolding as rapidly as in APAC markets."

-----------------------------------------------------------------------------------------------------------------------------------

Key Highlights:

APAC AS A STRONG GROWTH MARKET

While cloud computing has been the primary driver for DC demand, the rise of artificial intelligence (AI) is now fuelling a more explosive growth. The revolution in the scale at which data is being used and managed is fundamentally a global phenomenon, but nowhere is it unfolding as rapidly as in APAC markets. On population per MW basis, APAC markets are underserved compared to regions such as EMEA and North America[1].

APAC economies are not only growing faster, the region’s enormous population and swelling internet user base also cement its status as a highly attractive destination for DC investment. Its internet user base has grown seven-fold since 2005, compared to the growth of 1.9 times in the Americas and 1.8 times in Europe over the same period[2]. Going forward, APAC markets should continue to lead, as internet adoption further increases given the lower penetration rates in the region.

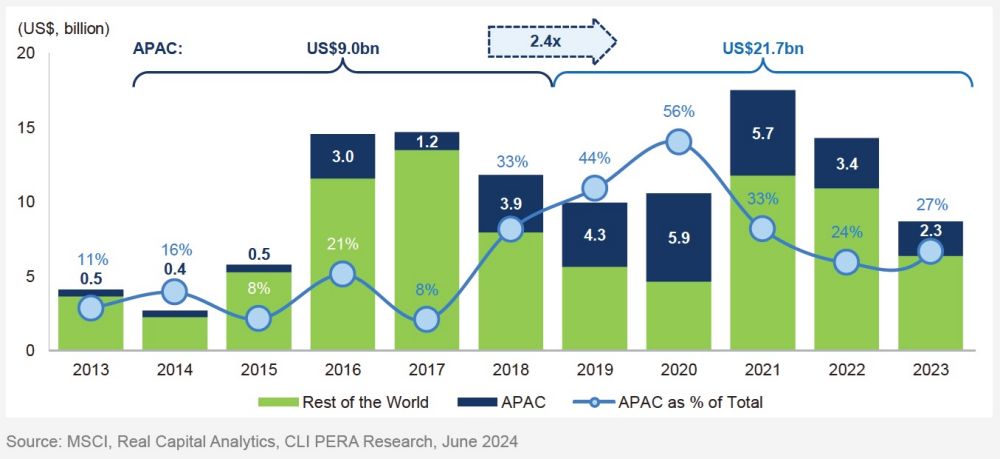

DC transactions in APAC rose about 2.4 times to approximately US$22 billion from 2019 to 2023, compared to the preceding five years, even as markets generally stagnated during the COVID-19 pandemic[3] [Figure 1].

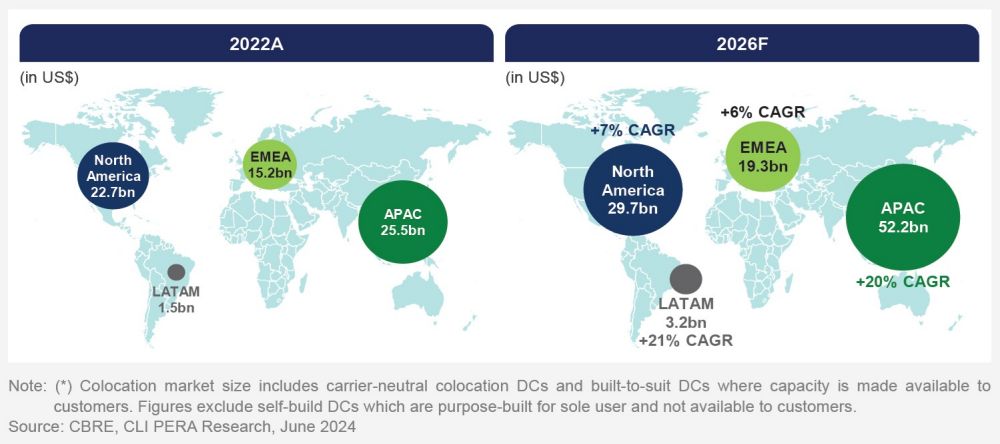

While hyperscalers continue to drive DC demand, APAC colocation market is also expected to double in size to US$52 billion by 2026[4], becoming the world’s largest colocation DC market [Figure 2].

KEY DC MARKETS IN APAC

Tokyo, Osaka, Seoul, Singapore and Sydney are key developed DC markets in APAC[5]. These markets have achieved scale and are important DC hubs in the region.

Beijing and Shanghai also show promise due to China’s large population, growing digital services sectors, strong government support, and robust long-term economic prospects.

INCREASING DEMAND FOR DCs IN INDIA

India has emerged as a hotspot for DC investment as a result of robust uptake of digital technology and a rapidly growing base of internet users. With the world’s second-highest number of mobile subscribers and one of its lowest internet penetration rates, market dynamics suggest the local DC industry has a long runway for growth.

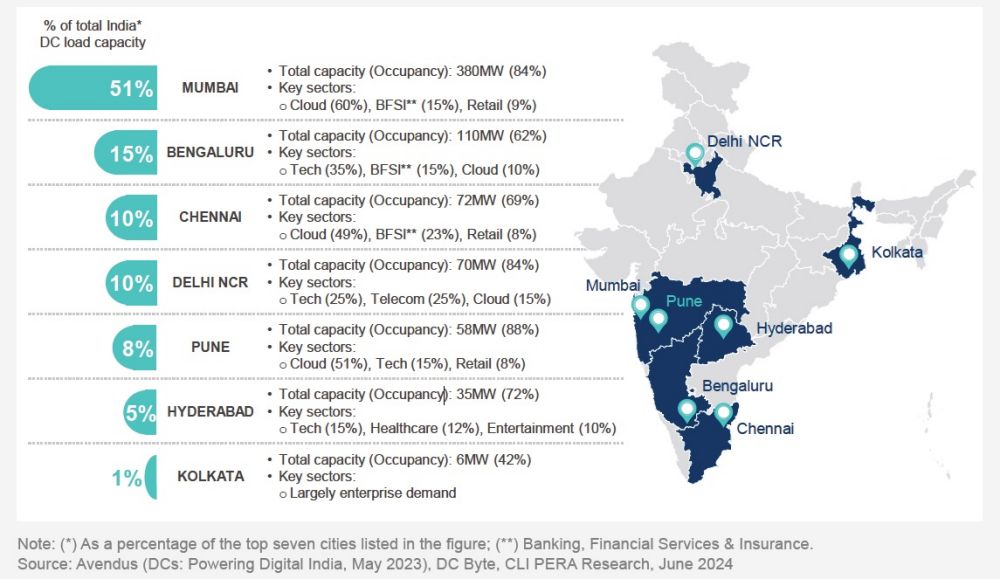

The seven major cities in India – Mumbai, Bengaluru, Chennai, Hyderabad, Delhi NCR, Pune, and Kolkata – are the focal points for new DC development, offering strategic locations with proximity to key business centres. Mumbai stands out as the preeminent hub, hosting more than half of the country’s DC capacity[6] [Figure 3] with the other major cities mentioned developing strongly.

While the Indian government’s focus on digital initiatives and economic reform has boosted transparency and created a more favourable business landscape, the challenges of operating in an emerging market underscores the importance of collaborating with a dependable local partner who can navigate the country’s regulatory complexities and offer opportunities to tap expertise in Indian DC networks.

OPPORTUNITIES AND STRATEGIC CONSIDERATIONS

Different DC models offer a spectrum of options for investors, catering to different preferences and risk appetites. However, the lack of stabilised DCs available for sale in APAC means the most promising opportunities for investors lie in developing new DCs – a strategy that can both satisfy new demand and yield higher returns.

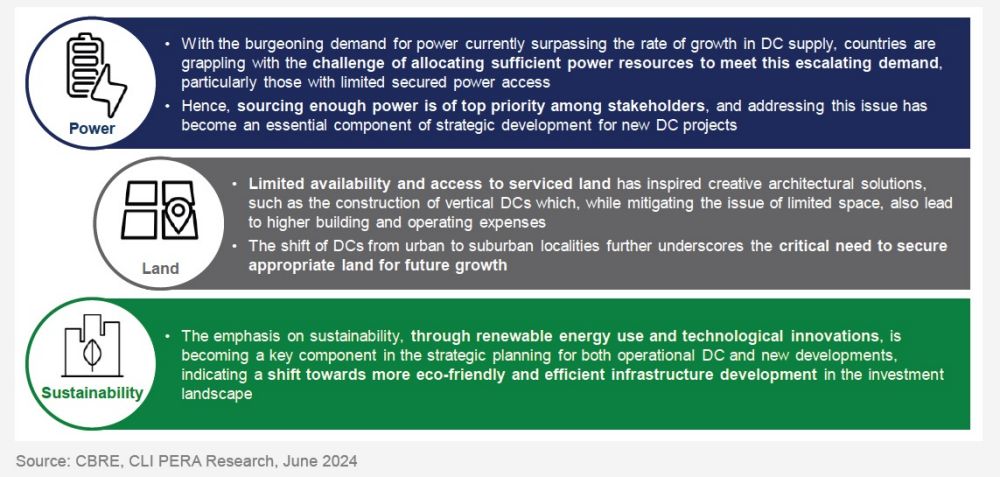

Power availability has taken centre stage as a crucial determinant for DC locations. There is also a growing emphasis on sustainability [Figure 4]. Increasingly, DC users and savvy operators are seeking to reduce their carbon footprints by being more energy-efficient and tapping renewable energy sources.

Investors should also be mindful of the geopolitical, regulatory and technological risks associated with DC investments. It is therefore crucial for investors to collaborate with DC partners who have a strong network, local expertise, and specialist domain knowledge.

--------------------------------------------------------------

Notes

[1] The World Bank, United Nations, CBRE, CLI PERA Research, May 2024.

[2] ITU World Communication, CLI PERA Research, May 2024.

[3] MSCI, Real Capital Analytics, CLI PERA Research, May 2024.

[4] CBRE, CLI PERA Research, May 2024.

[5] CBRE, Cushman & Wakefield, DC Byte, CLI PERA Research, May 2024.

[6] Avendus, “DCs: Powering Digital India”, May 2023, DC Byte, CLI PERA Research, May 2024.